A somewhat popular tactic of companies looking to improve their margins is to identify their low-margin customers and fire them. They don’t go Donald Trump on their customers and say “You’re fired.” Instead the companies jack up the prices of those customers to either drive them away or make them profitable. Some companies even erroneously think that is a pricing strategy. But is that really a profitable tactic? In our view, that tactic is often more harmful than helpful. The real answer is you need to understand much more about what the customers are buying, why the margins are low, and their incremental impact on profitability before changing their prices.

A somewhat popular tactic of companies looking to improve their margins is to identify their low-margin customers and fire them. They don’t go Donald Trump on their customers and say “You’re fired.” Instead the companies jack up the prices of those customers to either drive them away or make them profitable. Some companies even erroneously think that is a pricing strategy. But is that really a profitable tactic? In our view, that tactic is often more harmful than helpful. The real answer is you need to understand much more about what the customers are buying, why the margins are low, and their incremental impact on profitability before changing their prices.

Often times the suggestion to fire customers comes from the finance team as a result of an analytical review. In particular, it is fairly common for finance teams to look at the top and bottom 10% of customers in terms of gross margin or margin percent. It is easy to isolate the bottom customers and develop a plan to “fix them or fire them.” It is also common to review rate-volume-mix reports and identify customers with a product mix-shift to lower margin products, who are then candidates to be fired. A third source of targets for attention comes from looking at customer profitability reports generated by activity based costing (ABC) systems, and identifying the negative profit customers. All of these sources are worth looking at as starting points, but by themselves should never be a reason to significantly increase prices.

Gross margin on any given product is a function of what it costs the company to produce the product or service (fixed costs and variable costs), the demand for the product, the number and viability of competing alternatives, and the prices charged to customers. In every company, gross margin can vary from product to product or service to service based on a combination of those factors. Some products or services generate consistently higher margins than others, but even the low margin customers may be profitable.

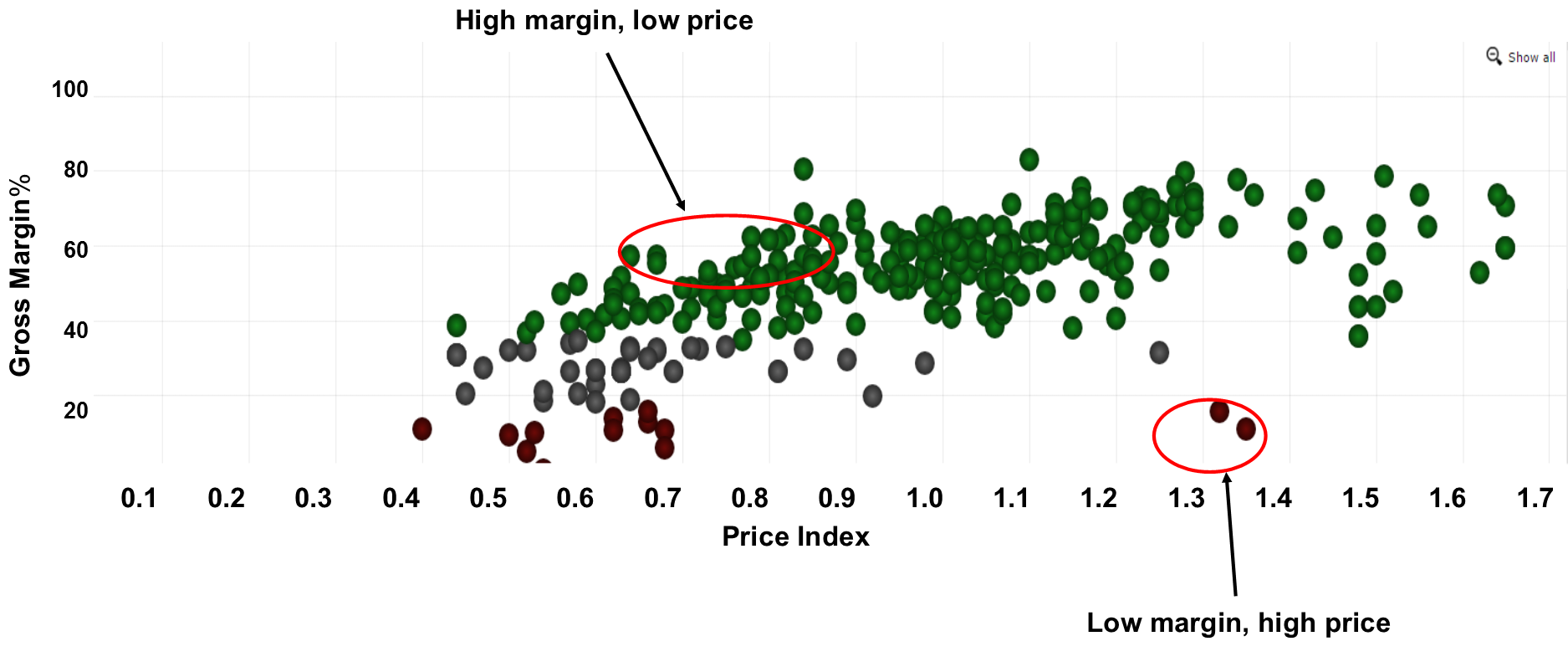

Beyond just looking at gross margin and product mix, it is important to look at how the prices of each customer compare to prices paid by others. In Figure 1 below, on the Y axis we have plotted gross margin, and on the X axis we show a price index, which is a measure of relative pricing. A price index above 1 indicates a customer is paying more than similar customers for a comparable basket of products or services.

Figure 1

It is fairly easy to identify some customers with relatively low margins who are paying more for their products than others. How? They are buying products that have an inherently low margin. Since they are already paying relatively high prices, jacking up the prices increases the likelihood that they leave. They fire themselves. But if those customers were contributing positive operating income, driving them away is exactly the wrong answer. Conversely if customers are generating low margins because they have low relative prices, by all means raise the price. There is a lower probability of those customers leaving simply because you begin to charge them what similar customers pay.

What if these low margin customers also appear in the negative profit report from your ABC model? Surely you should fire them in that case? Not necessarily. ABC models allocate all costs, including fixed and variable production costs and fixed and variable overhead. Before concluding that a customer is delivering negative profit, make sure you look at it incrementally. When Contribution Margin (Revenue minus variable costs) is positive and the customers’ relative price levels are high, you run a big risk of lowering your profits by driving the customers away with price increases. On the other hand, if their Contribution Margin is negative, some corrective action is required regardless of their price levels.

All of this begs the question of what to do about customers who buy a mix of products and services that is inherently lower margin, but they are paying relatively higher prices. First determine whether these customers could use the higher-margin products you offer, but are just buying them elsewhere. If so, lay out a sales plan to identify more specifically what their problems or needs are and how those are being better met by competitors. Then identify how you can do a better job of adding value or articulating your value to those customers and implement those steps.

If those customers are buying all the products they could buy from you at relatively high prices, but they simply have no need for your higher-margin offers – thank them for their business and accept they will be on your low-margin reports. But don’t raise their prices just because they appear on those reports. Firing low-margin customers may seem like the right thing to do and may even make you feel good about actively managing your customers. But it is the wrong answer if it actually worsens your profitability.